After heavy spending on developing LNG export capacity Oceania companies focus on expansion and backfill

Australia is well positioned to maintain its role as an important supplier of the world’s energy needs, particularly in the Asia-Pacific region. In 2017, Australia exported around 7 billion cubic feet per day (bcfd) of gas, equal to around 60% of production, with 46% of these exports going to Japan and 31% to China. Natural gas was the third biggest source of energy production in Australia in 2016-17, accounting for 23.1% of the total, behind coal and renewables. This was followed by oil and natural gas liquids (NGL) (3.3%) and liquefied petroleum gas (LPG) (0.5%), according to the Department of Environment and Energy (2018) Australian Energy Statistics.

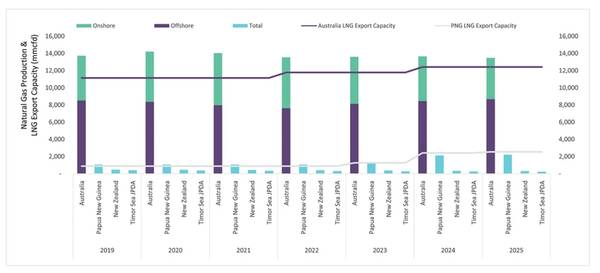

In 2018, natural gas represented 84% of Oceania’s hydrocarbon production in barrel of oil equivalent (boe) terms. Most of this production is from Australia, which is forecast to provide about 85% of the region’s natural gas production from 2019 to 2025. Australia’s liquefied natural gas (LNG) export capacity is forecast to be equivalent to 80% of the production in 2019 (Figure 1). Offshore production provides nearly two-thirds of the natural gas supply in Australia. While significantly smaller, Papua New Guinea’s output is expected to double over the period. Most of the gas production in Papua New Guinea is exported. Gas production is forecast to increase in line with LNG export capacity expansion, although companies will be required to reserve around 10% of gas production for domestic use.

Key upcoming Australian upstream projects

After completing a series of newbuild LNG export projects over the past five years, Australia has the largest LNG export capacity in the world. Australian operators are now turning their attention to developing assets to backfill the existing projects instead of investing capital expenditure (capex) in new LNG liquefaction capacity.

Three key offshore projects are the shallow water gas fields of the Caldita/Barossa asset and the deepwater Scarborough and Browse developments. These developments are yet to be sanctioned, but will be crucial for Australia to maintain supply to the LNG export projects.

The Caldita/Barossa project is around 300km north of Darwin. Development of Caldita/Barossa is expected to utilize a floating, production, storage and offloading (FPSO) vessel with subsea wells, exporting gas to backfill the Darwin LNG plant. The Scarborough gas field is located in the Carnarvon Basin, 375km offshore Western Australia at around 900 meters water depth. Development of Scarborough includes a semi-submersible platform, with subsea wells, exporting gas to support an expansion of the Pluto LNG facilities.

The largest project under discussion is Browse, which aims to bring online the Brecknock, Calliance and Torosa fields offshore West Australia. The project has been stalled for a few years, with greenfield onshore and floating LNG proposed and ruled out, and it is now expected to follow a similar pattern to the other projects, utilizing two FPSOs, with subsea wells and backfilling the existing North West Shelf (NWS) LNG trains.

Liquids production in Australia has fallen from 29% of production to 16% on a boe basis, due to the focus on natural gas for LNG export and the lack of oil discoveries.

The shallow water Dorado oil discovery last year by Quadrant Energy (now acquired by Santos) and Carnarvon Petroleum is a significant boost for the region.

The discovery is reported to hold 2C resources of 186 million barrels of liquids and 552 bcf of gas. This is relatively small on global scale, but is the largest liquids discovery for over 30 years in the North West Shelf area. It could spur further exploration and liquids focused developments nearby.

| Table 1: Key Announced Offshore Australia Projects | |||||||

|---|---|---|---|---|---|---|---|

| Field | 2C Resources (tcf) | Production Target (mmcfd) | FID | Production Start Year | Operator | Upstream Development Capex (USD) | LNG Plant |

| Caldita/Barossa | 3.44 | 470 | 2019 | 2023 | ConocoPhillips | 1,400 | Darwin |

| Scarborough | 7.3 | 1,000 | 2020 | 2023 | Woodside | 6,300 | Pluto |

| Browse | 15.4 | 1,270 | 2021 | 2026 | Woodside | 22,000 | NWS |

| Source: GlobalData Oil & Gas Intelligence Center | |||||||

The Author

Nicole Zhou is an upstream analyst at GlobalData, primarily covering upstream asset valuations and forecasts in the Asia-Pacific region. She holds an MSc. in Petroleum Engineering and previously worked as a drilling engineer for ConocoPhillips in China and as a Commercial Lead for Hilong Oil and Gas Service Company.

Subscribe

Subscribe