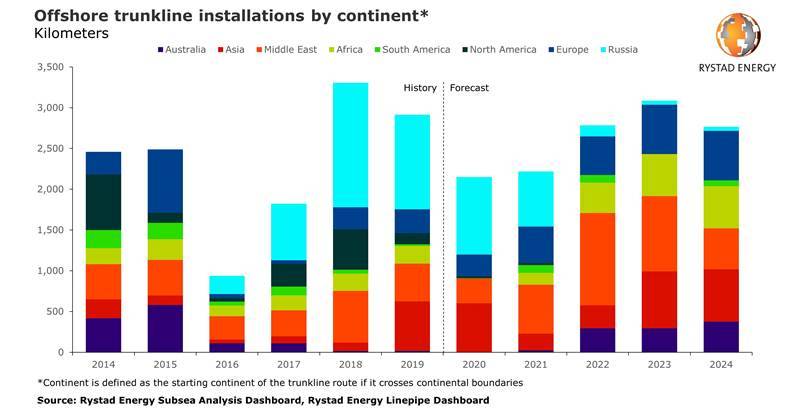

Norwegian energy intelligence company Rystad expects that the market demand for large-diameter offshore pipelines, known as trunklines, will see an annual drop of 26% this year.

According to Rystad, the length of total installations this year is forecasted to reach 2,150 kilometers, down from last year’s 2,913 kilometers.

While the demand is expected to drop, Rystad says that this downturn’s impact on trunkline demand is, however, lighter than that of 2016, and recovery is likely to be swift, led by projects in the Middle East.

"Although it is set for a significant drop from last year’s 2,913 km, offshore trunkline demand is holding up much better now than during the previous downturn, when demand plummeted to just 938 km in 2016 from 2,488 km the year before," the Norwegian company said.

As for the recovery in demand, Rystad Energy estimates that projects in the Middle East will propel demand to almost pre-Covid-19 levels already from 2022 and push it even higher from 2023, when offshore trunkline installations are projected to exceed 3,000 km.

"The offshore trunkline market will recover to its prior levels in the next few years, driven by a handful of large transmission lines between regional markets and numerous export lines from upcoming offshore gas field developments,“ says Henning Bjørvik, energy service analyst at Rystad Energy.

The global trunkline market is divided into upstream export lines connected to processing or production facilities, and transmission lines used for downstream transport between regions and markets. Although connected, the market drivers and characteristics of the two trunkline types are quite different, Rystad says.

Demand for export lines, Rystad explains, is directly related to offshore upstream development activity, where primarily gas field developments call for trunklines. Transport infrastructure accounts for a significantly larger portion of the value chain for gas developments than for oil, where operators can opt for export via buoy loading onto oil tankers. In project count terms, more than 90% of the nearly 100 offshore trunklines expected to be developed in the 2020–2024 period are gas export pipes.

Transmission line projects are more loosely connected to field developments, Rystad says.

"They normally originate in giant field development clusters that produce more gas than needed in local markets and can stretch out several hundred kilometers to reach import markets. Transmission line projects are often highly unpredictable due to geopolitics, and route decisions and legal approval stages are lengthy processes, especially for cross-country lines," Rystad adds.

Transmission lines make up around half of the new trunklines forecasted up till 2024 measured by length, but in project count they amount to less than one third. As a result, alterations in the timing of a few of these can throw the market around quite a bit, Rystad says.

Capacity Dwarfs Demand. Prices to remain low

According to Rystad, recent trunkline demand in Europe/Russia has been dominated by the contentious Nord Stream 2 dual transmission lines from Russia to Germany across the Baltic Sea, where installation started in 2018.

Halted by existing US sanctions, 160 km of the 2460-km, 48-inch project remain to be laid and Rystad Energy expects the project to be completed in 2021. North Sea oil and gas export lines have also contributed to demand.

Going forward, the EastMed transmission pipeline spanning the Mediterranean Sea from Israeli waters via Cyprus to mainland Greece is the largest driver in kilometer terms with offshore sections totaling 1,340 km expected to be installed between 2023 and 2026, Rystad says.

According to Rystad, the Middle East trunkline market will continue to be dominated by export lines associated with giant offshore developments in Iran, Saudi Arabia and Qatar, while Asia-Pacific demand will be led by Australian export lines such as Barossa, Scarborough and Browse LNG. African projects contributing to trunkline demand include Egypt’s Mediterranean Zohr field and the Mamba development in Area 4 off Mozambique, while the Americas is the only market expected to see a decline in installations in the coming years.

"Despite the improving demand outlook for transmission lines, prices for the pipes themselves are expected to remain under pressure for the foreseeable future due to excess capacity in the global market for large-diameter linepipe manufacturing," the company said.

“Capacity still dwarfs demand, so even when demand picks up, we tend to find that there are always pipe mills with spare capacity that will offer competitive pricing to win orders so they can boost their utilization rates,” says Rystad Energy’s Senior Vice President for Energy Service Research James Ley.

Subscribe

Subscribe