The market for offshore support vessels has experienced tremendous development in the last couple of years. And while we expect the market to continue its positive journey, we would argue that, at least on an overall basis, the market has already recovered to healthy levels at the time of writing.

There are solid underlying fundamentals that are driving the increased vessel demand, chief among them is the increased offshore upstream investment on a global level. Overall, spending on exploration and production is set to increase roughly 45% from 2021 to 2025, reaching a total of almost $200 billion in the latter year.

Although this increased spending has translated into increased offshore activity as a whole, it should be noted that it has not hit all vessel segments equally, even among offshore drilling rigs. In fact, while the number of jackup drilling rigs under contract has risen in accordance with increased investments, the same cannot be said for floating drilling rigs.

As such, the OSV demand derived from E&P drilling has developed accordingly, where benign and shallow-water regions, typically dominated by high volume yet low capacity AHTS units, have seen the largest increase in terms of incremental demand. For deepwater and ultra-deepwater regions, we record a transition towards high-capacity ships, although herein we also take note of a significant shift to subsea field developments as opposed to conventional infrastructure.

Finally, as several offshore oil and gas regions have and will come into maturity, we register that there is a relatively higher growth for production support more than exploration derived operations, thus favouring assets focused on the former. These trends both have and will continue to shape the vessel landscape as the ongoing trends are expected to persist for the foreseeable future.

North Sea Demand Flat, While Other Regions Record Rise

The implications thus vary depending on the region in question, and in the North Sea basin, for example, we find that vessel demand has remained stagnant with flat development in recent years. Moreover, the increased dayrates herein has come about as a result of fewer vessels both active and in the fleet as a whole, and in fact, the current OSV fleet in this region is at its lowest in well over a decade.

In both the Southeast Asian and Middle East regions the opposite is true, wherein the number of working units has grown significantly, and the latter is currently at an all-time high level. Despite this, dayrates in the Persian Gulf has yet to materialize to the same degree as seen elsewhere. Granted, this is in large part due to the sever market share of government-controlled players throughout the supply chain, yet also as a result of persistently high vessel availability for most asset classes.

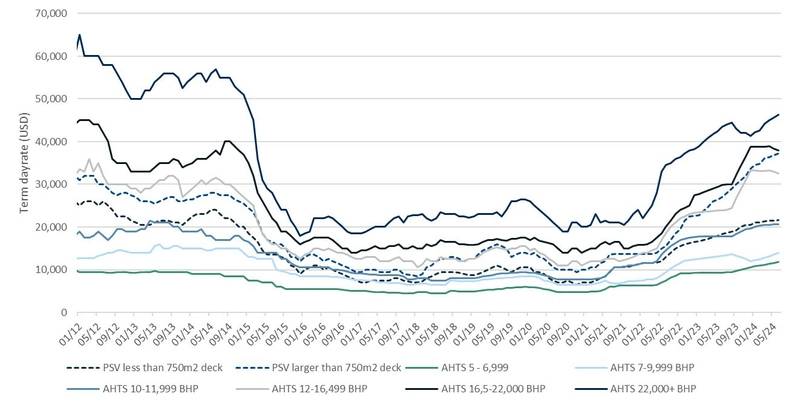

In both Brazil and off West Africa on the other hand, the dayrates has increased tremendously thus far in the upcycle brought on by a combination of both a distinct lack of suitable tonnage as well as higher vessel demand. Moreover, as these areas are facing a shortage of local vessels to support the activity hikes, we have seen a large number of ships mobilized from other regions, offering lucrative opportunities for international OSV owners. OSV Term Rates Graph (Credit: Fearnley Offshore Supply)

OSV Term Rates Graph (Credit: Fearnley Offshore Supply)

To this effect, the average dayrates for all asset classes has increased significantly, and as seen on the graph, several of which are now well above previous peak levels. Furthermore, given the large number of planned project developments and drilling campaigns in both regions, and with next to no new supply added in the near future, we expect continued upward pressure on rates overall.

Another OSV Newbuild Boom Not on the Horizon ... Just Yet

Historically, we as an industry have spoiled our own party by ordering far too many OSVs which then adds insult to injury in the ensuing downcycles. But even in the absence of a demand crash almost ten years ago, the market forces saw the newbuild orderbook bloated even compared to the then peak activity demand.

Could our current market cycle really be any different; have the market players burnt their fingers enough times that this time they do not repeat themselves? We certainly hope so, but either way there are a number of important reasons why we do not believe there will be another newbuild boom akin to what we have seen previously.

However voluntary or not the current newbuild ordering, or lack thereof, matters not, but what does matter is the cost and lack of available capital towards this end. It is a fact that the majority of the largest financial institutions that fuelled the previous ordering sprees have either exited entirely or significantly reduced their exposure to oil and gas.

The same is true for the availability of yard slots suitable for OSVs. On one end, the total capacity of such shipyards has been heavily reduced since the last run-up, especially in the Far East. But even more so, in the absence of OSV orders, the shipyards that are in operation have certainly not idly waited for the return of the market.

Other vessel segments, such as support vessels for offshore wind and commercial fisheries and aquaculture are all built at yards that used to build PSVs and AHTS. As such, there is currently a very limited number of slots left for anyone looking to place an OSV newbuild.

More to that point there are also severe supply chain constraints presently impacting the industry, especially concerning people and a wide range of equipment including diesel generators and engines. As a result of this, the build time for offshore vessels is currently between 24 and 36 months depending on the asset type. This, in combination with the abovementioned factors, all contribute to increased costs as well.

Finally, there is inherent technological risk associated with ordering a newbuild at this point in time, especially so when ordering on a speculative basis. While there are many good arguments for switching to low- and zero emission fuel alternatives, there is currently no market consensus towards just what fuel will be widely adopted by the industry. Choosing the wrong fuel today could have a negative impact on the vessels’ operability in the future, and there are different preferences, not just amongst operators and charterers, but also in between regions.

All in all, we find it difficult to imagine another newbuild boom on the horizon from where we are standing, at least one similar to what we have seen before. In light of this, we remain firm in our upbeat expectations for the OSV market going forward, where both dayrates and vessel activity are expected to continue to rise for years to come.

Subscribe

Subscribe