Floating systems consultant Peter Lovie offers his personal take on the debt crisis facing round FPSO pioneer Sevan and the unexpected challenges encountered by the US Gulf of Mexico's first FPSO .

Sevan brought the first round FPSOs into operation. While the Norwegian company may not have been the first to have thought of the round FPSO concept, it was the first to successfully develop and commercialize it. That's a remarkable achievement, for it is tough to get a novel production facility concept accepted because it requires an oil company to dedicate a field to the new technology. Success for both parties hinges on much.

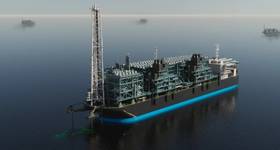

Sevan's Voyageur FPSO operating at Premier Oil's Shelley field in the North Sea.

Sevan's Voyageur FPSO operating at Premier Oil's Shelley field in the North Sea.One hot issue these days in the FPSO community is what is going to happen to Sevan when it emerges from a debt crisis stemming from a number of factors, including cost overruns on the modifications to the Voyageur FPSO. But first, some history.

Sevan brought Piranema, the first round FPSO, online in October 2007, serving Petrobras in the Piranema field in 1090m of water offshore Brazil (OE December 2008). Hummingbird followed in August 2008 at Centrica's Chestnut field in the North Sea in 120m of water.

Two drilling units were contracted using Sevan's round hull design. One has been operational in the Campos Basin, drilling for Petrobras since mid-2010 (OE July 2010), while the second is under construction, also contracted to Petrobras. The drilling business is now split out in a separate company: Sevan Drilling.

A larger version of the Sevan FPSO with 1 million barrels storage capacity is under construction at the Hyundai yard in China for the Eni-operated Goliat field in the sub-arctic Norwegian Barents Sea .

The Voyageur FPSO operated for Premier Oil in the UK North Sea from March 2009 at the Shelley field in 95m water depth. During operation at Shelley, Sevan was contracted by E.ON Ruhrgas to redeploy Voyageur to the Huntington field in 90m of water in the UK North Sea under a new firm five-year contract. The move meant conversion work to suit the new site: upgrades of two gas compression trains for gas export and gas lift as well as an increase in the water injection system. The budgeted $90 million ballooned to possibly be as much as $170 million.

In the early riskier years of Sevan's corporate development, as one might anticipate, it seemed there had been relatively little capital recovery. Being hit with overruns on top of other commitments created a business-threatening financial storm.

Construction overruns have commonly afflicted the FPSO business in both first construction as well as in redeployments. Sevan's current troubles chime with issues encountered by Bluewater when redeploying its Glas Dowr FPSO from the North Sea to South Africa in 2002. It should have been a fairly routine project, calling for adapting the vessel to a new location and meeting production requirements such as additional compression, like Sevan faced. Instead it ended up taking overruns of some months and budget to the tune of approximately $195.7 million, versus $50.4 million reimbursable by the customer. Fortunately for Bluewater, the company was not in as financially tight a situation as Sevan.

Other companies have designed round FPSOs, but struggle in maturing their technology to the point where an operating oil company will take the plunge that Petrobras took with the Piranema FPSO. During my time in the project management office at Devon Energy, as with other oil companies we looked at development solutions from various FPSO companies: Sevan, SSP, MONOBr and Deepwater Structures in addition to traditional ship-shaped FPSOs. Our assessments were not just focused on technical design but the complete picture of finding a matured concept that could be reliably built and meet all operational considerations – such as the disconnectability needed in the Gulf of Mexico, export to tankers or pipe – versus other proven and competing development solutions on the table such as TLPs, semisubmersibles and spars.

Recently, the technology maturity question has seen increased critical attention by oil companies, with the petroleum industry now using a seven-stage Technology Readiness Level scale. On that scale, Sevan's design is proven in the field and qualifies at TRL 7, while the other untried round FPSO designs that have done model tests and many paper studies correspond to about TRL 2 if that scale is literally applied. That's a difficult gap even for super salesmen to overcome with typically risk-averse operators.

Quiet Cascade

If you want to know what's really happening with the first FPSO in the US sector of the Gulf of Mexico, well, you're going to have ask the operator – Petrobras America in Houston. Both Petrobras and its FPSO contractor – BW Offshore – have been unusually tight-lipped about progress in bringing the BW Pioneer FPSO onstream to serve the Cascade/Chinook fields.

Nevertheless, one can easily enough assemble a lot of ‘circumstantial evidence' on where things stand with the first FPSO to be approved for production in the US Gulf.

BW Pioneer will serve Petrobras at Cascade/Chinook.

BW Pioneer will serve Petrobras at Cascade/Chinook.The spread of the FPSO plus the two associated shuttle tankers needed for the Cascade/Chinook development was contracted in 3Q 2007. Petrobras as operator did a remarkable job in assembling bids and negotiating contracts for these pioneering vessels: a fiveyear minimum charter on the FPSO. The FPSO would be in a record water depth of 8200ft and faced the hurdles of being the first to be approved in the US Gulf of Mexico despite the industry effort in getting the generic Environmental Impact Statement prepared and a record of decision being made in favor of FPSOs back in December 2001. It was made more difficult on the shuttle tanker side as that was then and still is a narrow and expensive market, made so by America's notorious Jones Act! Despite all that, Petrobras America and its partners at the time sought an FPSO as the preferred solution for the field.

I was in the middle of it all as senior advisor floating systems for Devon Energy, then a 50:50 partner with operator Petrobras on the Cascade field in the Walker Ridge area. When Devon exited deepwater entirely in 2H 2009, that block became 100% Petrobras-owned and operated. With Petrobras holding a two-thirds interest in the adjacent Chinook field (Total has the remainder), the Brazilian company became more exposed than ever in that pioneering development.

Fast forward to April 2010, when BW Pioneer arrived in the Gulf scant weeks before BP's Macondo disaster. Talk about incredibly tough timing. The first shuttle tanker became available, and now – more than a year later – so has the second, sitting in Rio de Janeiro at the time of writing. But there's no work in the US Gulf for either of them. The first saw some service at Macondo and is reported in Brazil, presumably building US crew experience – like the second shuttle tanker – in the course of interim offloading work until they can return to their original US objectives. Day rates on these Jones Act compliant shuttle tankers are much higher than international flag shuttle tankers of equal capacity – an unexpected expense for the operator when these tankers are not at their intended Gulf duty.

The drilling program on Cascade, critical to define the reservoirs, became subject to the US government's drilling moratorium in 2010 and was stopped. Next, Petrobras America faced more troubles in 2011, with stories of a chain link breaking and the riser buoyancy can popping to the surface – more checking and delays pushed first oil from 2Q to 4Q 2011.

The whole purpose of using an FPSO at this particular development was to start production earlier and mitigate risks at a project that would produce from untried formations in a remote area. The oil price deck today in 2011 may be different, perhaps better from sanction time in 2007, but with all these acts of god and man from April 2010 to date, the overall NPV10 economics for the development would be different. No one in 2007 could have forecast how it would work out in 2011!

It certainly has been a challenging time. I hope one day we can get the full story from Petrobras America – they deserve great respect for dealing with all they have had to face in developing this project and in persevering in the face of one adversity after another. OE

Peter Lovie, a fellow of the Royal Institution of Naval Architects and a registered professional engineer in Texas, was educated at Glasgow University and earned his Master of Applied Mechanics as a Fulbright Scholar at the University of Virginia. Based in Houston, he has held senior management posts with Bluewater and American Shuttle Tankers (now Teekay) before joining Devon Energy in 2006. He now works as a floating systems consultant as well as serving as EVP of SO COSS Global, a Houston start-up company developing a portfolio of projects for West Africa.

Subscribe

Subscribe