Dutch FPSO leasing specialist SBM Offshore has completed the project financing of FPSO Sepetiba for a total of US1.6 billion, which SBM Offshore says, is the largest project financing in the company’s history.

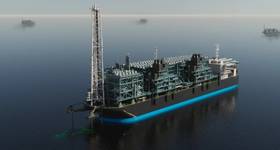

FPSO Sepetiba, formerly known as Mero 2, is destined for deployment in Brazil with Petrobras.

SBM Offshore said that the project financing was secured by a consortium of 13 international banks with insurance cover from Export Credit Agencies (ECA): Nippon Export and Investment Insurance (NEXI) and SACE S.p.A. A letter of intent was received from China Export & Credit Insurance Corporation (Sinosure) which intends to join this transaction by the end of the year and will replace a portion of the commercial banks’ commitments, the Dutch floating production firm said.

The loan is composed of four separate tranches with a 4.3% weighted average cost of debt, a fourteen-year post-completion maturity for the ECA covered tranches and a fifteen-year post-completion maturity on the uncovered tranches.

FPSO Sepetiba is owned and operated by a special purpose company owned by affiliated companies of SBM Offshore (64.5%) and its partners (35.5%).

The vessel will have a processing capacity of up to 180,000 barrels of oil per day, a water injection capacity of 250,000 barrels per day, an associated gas treatment capacity of 12 million standard cubic meters per day, and a minimum storage capacity of 1.4 million barrels of crude oil. The FPSO will be spread moored in approximately 2,000 meters water depth.

The unit will be built under SBM’s Fast4Ward program, which incorporates a newbuild, multi-purpose hull combined with several standardized topsides modules, and is expected to be delivered in 2022.

FPSO Sepetiba will be deployed at the Mero field in the Santos Basin offshore Brazil, 180 kilometers offshore Rio de Janeiro.

The Libra block, where the Mero field is located, is under Production Sharing Agreement to a Consortium comprised of Petrobras, as the operator, with 40 percent, Shell Brasil with 20 percent, TotalEnergies with 20 percent, CNODC with 10 percent and CNOOC Limited with 10 percent interest. The consortium also has the participation of the state-owned company Pré-Sal Petróleo SA (PPSA), as manager of the Production Sharing Contract.

Subscribe

Subscribe