After a slowdown in activity during 2020/2021 due to soft commodity prices, demand for FPSOs is picking up.

With exploration hotspots like Namibia’s Orange Basin and the East Mediterranean delivering new finds, the FPSO market outlook is healthy. But shipyard capacity constraints are beginning to weigh on delivery, leading to cost concerns. Furthermore, FPSO demand is competing for yard space with other construction projects.

To mitigate delay risk and cost overruns, some E&Ps have reviewed their FPSO procurement strategies. The Build Operate and Transfer (BOT) model and use of standardized hull designs are becoming more popular.

Strong Demand But Capacity Constraint Headwinds

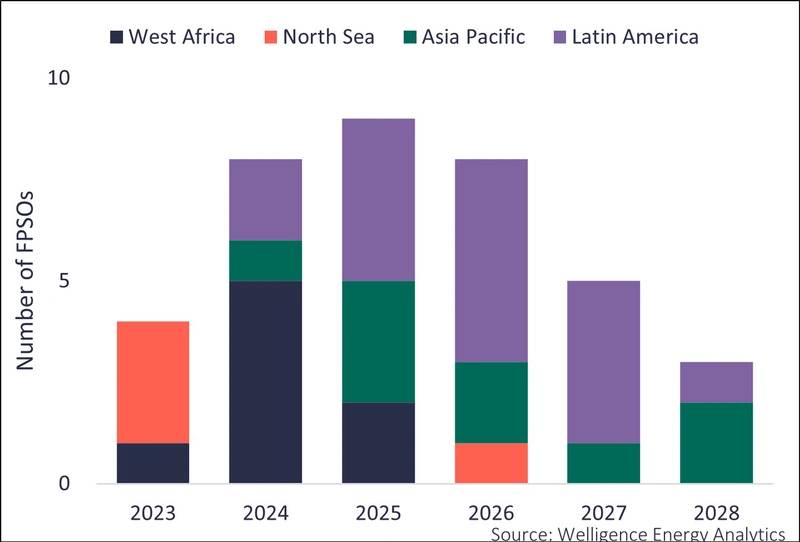

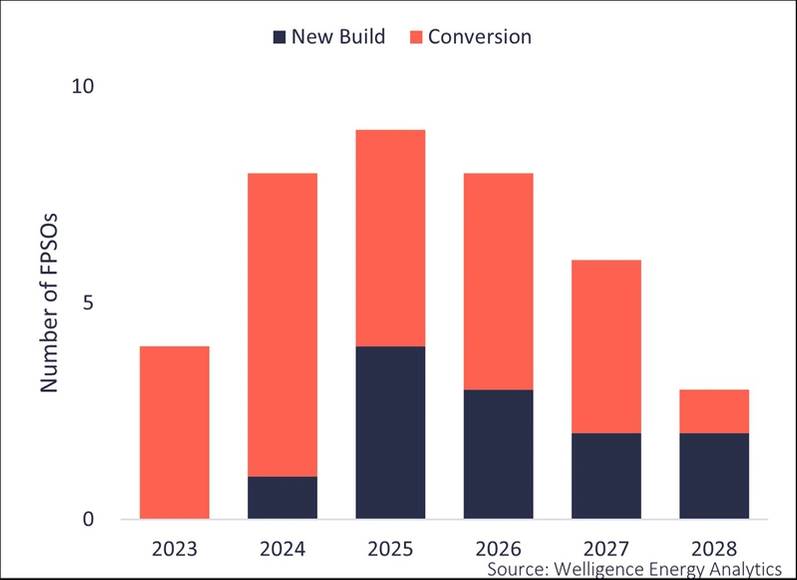

We expect 35 FPSO projects with an estimated contract value exceeding US$50 billion to get the green light by 2030. At least a third will be new builds, and nearly half earmarked for Brazil and Guyana. The next hotspot could be Namibia, where TotalEnergies and Shell’s exploration success could yield multi-FPSO development programs. The yards in China are the go-to for new-build FPSO hulls and conversion work, but capacity is strained.

FPSO demand forecast (by region): Demand is based on FPSO contract award year

FPSO demand forecast (by region): Demand is based on FPSO contract award year

Title FPSO demand forecast (by region): Demand is based on FPSO contract award year

Title FPSO demand forecast (by region): Demand is based on FPSO contract award year

Although new FPSO demand will not be as overheated as in 2014/2015, hull fabrication is now competing for yard space with other projects like FLNG vessels, floating regasification units and wind turbine installation vessels.

China Dominates FPSO Hull Fabrication Market

Historically, the large drydocks (Samsung, Daewoo, Hyundai) in South Korea built the majority of the large, complex FPSOs. But they have been surpassed by the Chinese yards, which have beaten them on price and delivery time. On the conversion side of the market, Singaporean yards like Semcorp and Keppel dominated, but also now face strong competition from China.

E&P Procurement Strategies Evolve

The main FPSO contracting models have been turnkey (used for large, new-build FPSOs) or lease contracts (used for VLCC conversions). But the Build Operate and Transfer (BOT) model is becoming more popular, as is the use of standardized hull solutions.

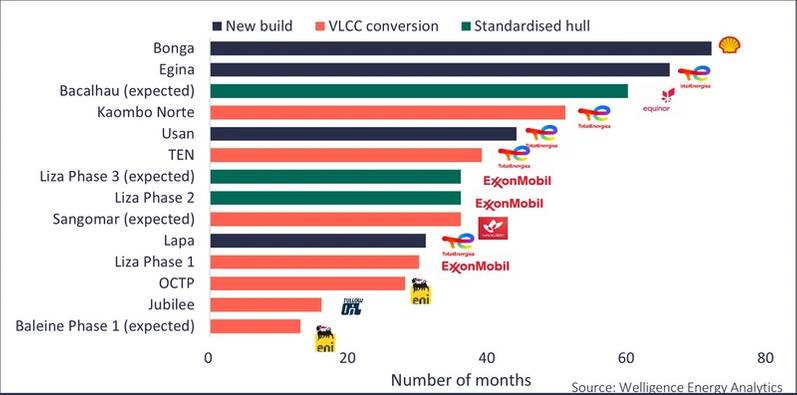

Lead time for FPSO projects operated by selected IOCs (FID to first oil)

Lead time for FPSO projects operated by selected IOCs (FID to first oil)

Equinor’s Bacalhau FPSO will use combined cycle turbines, and more operators will likely go down this path. Aker Carbon Capture is developing an FPSO carbon capture solution, and it’s reported this technology will be deployed on two Petrobras FPSOs. However, there is a cost – we estimate the combined cycle gas turbine will increase the topside costs by 20-30%.

Subscribe

Subscribe