In announcing project sanction on the Scarborough and Pluto Train 2 project last week, Woodside CEO Meg O’Neill emphasized that as well as being both low carbon and globally cost-competitive, it was the strength of demand “particularly in our markets in Asia” that underpinned the US$12 billion investment. I couldn’t agree more, especially with the region’s whopping 21 Mt of LNG demand growth this year putting to bed any fears about a recovery in Asian gas demand after a wobbly 2020.

Indeed, it is confidence in the resilience of long-term Asian gas demand, even in our accelerated energy transition scenarios, that has been key to the 50 mmtpa of new LNG supply that has taken FID in 2021 compared to only 3 mmtpa in 2020. Good news for the global LNG industry, but suppliers must still do more: nothing short of a new industry manifesto, laser-focused on reducing emissions to deliver a far greener product, is required if LNG is to secure a sustainable future and bolster longer-term Asian demand.

The rise (and rise) of Asian LNG demand

For decades, Asia’s rapid economic growth meant unchecked hydrocarbon demand – mostly coal and oil. With tackling emissions now firmly on the political agenda, this is unwelcomed, unsustainable, and should open the door to greater use of gas.

Hence, what really excites LNG developers today is an Asian LNG demand story that isn’t simply about GDP forecasts but more attuned to carbon reduction goals and aligned with energy strategies; new policies favoring gas over coal in power generation are creating additional opportunities for buyers across the region, especially in Northeast Asia; depletion of domestic gas supply is encouraging LNG imports in the Philippines, Thailand, and Vietnam; gas market liberalization in South Korea, Thailand, Singapore, and Malaysia is attracting new investors. Furthermore, new infrastructure is being built in China and across South and Southeast Asia to support continued growth in gas.

China is the star of the show (with a shoutout to South Korea), with strong policy support providing clearer scope for LNG demand growth. Imports are up 13 Mt this year alone. And with regasification capacity expected to double by 2025, we now forecast imported LNG demand to be almost 100 mmtpa by 2025, some 8 mmtpa above [Wood Mackenzie's] previous view.

Amidst the euphoria, it’s worth a reality check. Omicron is a blunt reminder that coronavirus is more than capable of shredding confidence in a matter of days. Strong nuclear generation is further reducing LNG requirements in Japan, and South Korea is moderating imports based on record high inventory levels. Rising domestic offshore gas production in India is also slowing the pace of LNG demand growth. The LNG industry is all too aware that short-term projections can be fickle.

The return of the long-term contract

Supported by demand growth has been a rebound in LNG contracting activity after a slow 2020. While we still expect companies in the market for long-term contracts starting after 2025 to be spoilt for choice, sky-high spot LNG prices and resurgent demand have seen buyers reaching for the security blanket: more than 28 mmtpa of new contracts have been signed so far in 2021, the highest volume since 2016.

As my colleague Dan Toleman notes in his recent analysis of LNG contracting trends, Chinese buyers have been incredibly active this year. Among the NOCs, CNOOC‘s SPA with Qatar Petroleum was followed by Sinopec and Sinochem concluding long-term offtake deals with US LNG developers. Emerging Chinese buyers have been similarly prolific, with Shenergy Group, Zhejiang Energy Group, and ENN leading the way with SPAs that aggregate 65 Mt of LNG. Elsewhere, Pakistan State Oil and buyers in Bangladesh have also been active, picking up three new long-term contracts. And in Singapore, Pavilion Energy signed a deal that will deliver 8 Mt over 10 years.

The next wave of LNG FIDs

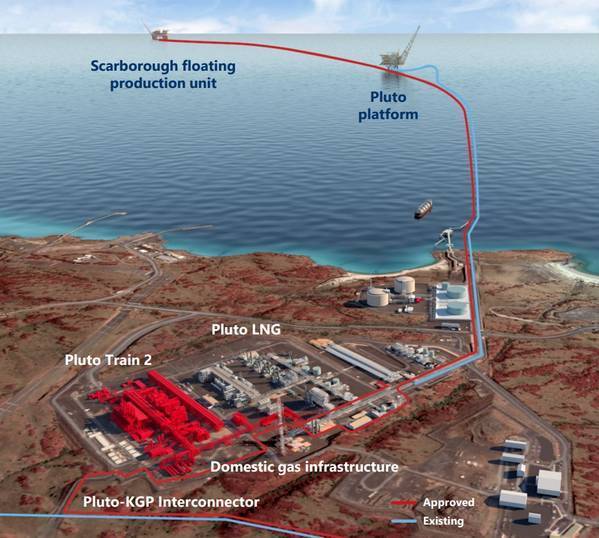

Asia’s appetite for LNG contracting is manna from heaven for pre-FID projects. 2021 is proving a bounty year after a skinny 2020, with project sanctions this year in Qatar (North Field East), Russia (Baltic LNG) and Australia (Scarborough/Pluto 2).

As the siren call of Asian LNG demand grows louder, more will follow. Over the next 12 months, we expect several low-cost projects to move towards sanction including Cheniere’s Corpus Christi Stage 3 and Venture Global’s Plaquemines project in the US, North Field South in Qatar, and Arctic LNG-1 in Russia.

But this window won’t remain open indefinitely. Much of the LNG sanctioned in 2018 and 2019 is now expected post-2025, resulting in abundant LNG supply coming to market in the 2026-28 period. Qatar’s expansion and Russia’s Baltic LNG then mop up most of the remaining contestable demand during this period, setting the scene for renewed price pressure. US developers in particular will be rushing to expedite new projects.

Asia is supporting stronger-for-longer LNG prices

The price recovery we had already expected in 2021 clearly hit harder than anticipated. And while prices will inevitably soften through the back end of the winter, fundamentals point to stronger-for-longer LNG prices. Despite falling from recent highs, European prices remain volatile and high charter rates and Panama Canal bottlenecks will keep the Asian premium in place through much of the coming year.

Looking further out, limited LNG investment between 2015 and 2017 will bite as increasing Asian demand is set to reduce LNG availability to Europe. Combined with less LNG supply growth than previously forecast as projects under construction in Canada and Africa signal delays, we now see gas prices at higher levels than had been expected through to 2025.

The call for greener LNG is being heard

But rising Asian gas demand doesn’t mean easy pickings for LNG suppliers. In response to net zero targets across Asia, it will be those projects that move first and move fastest on reducing emissions that move forward.

"With stakeholders across Asia increasingly calling for more action on carbon, developers now must go further in reducing Scope 1 and 2 emissions, as well as respond to calls for greater transparency and certification around carbon emissions (despite there still being no industry standard for this). Some are going further, including partnerships with customers on tackling Scope 3 emissions. The prize for those who succeed is the Asian gas market.

The Author

APAC Energy Buzz is a weekly blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Thompson shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.

Subscribe

Subscribe